Table of Contents

ToggleHow Businesses Can Benefit from the Nation’s EV Charging Support Ecosystem

India is aggressively transitioning to electric mobility, and government policy frameworks are central to building a robust EV charging ecosystem across the country. For EV charger manufacturers, installers, charge point operators (CPOs), and commercial partners, understanding these incentives is crucial for maximizing returns and accelerating deployment.

Let’s break down the latest policy structures, financial support schemes, state incentives, and how businesses can leverage them for profitable growth.

National EV Policies and Charger Incentives

PM E-DRIVE: The Successor to FAME-II

The PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-DRIVE) scheme, launched in October 2024 and operational through March 2028, is India’s flagship EV support policy. It replaced and expanded the earlier FAME-II scheme with a broader focus on vehicles and charging infrastructure.

Key highlights:

Total outlay: ₹10,900 crore.

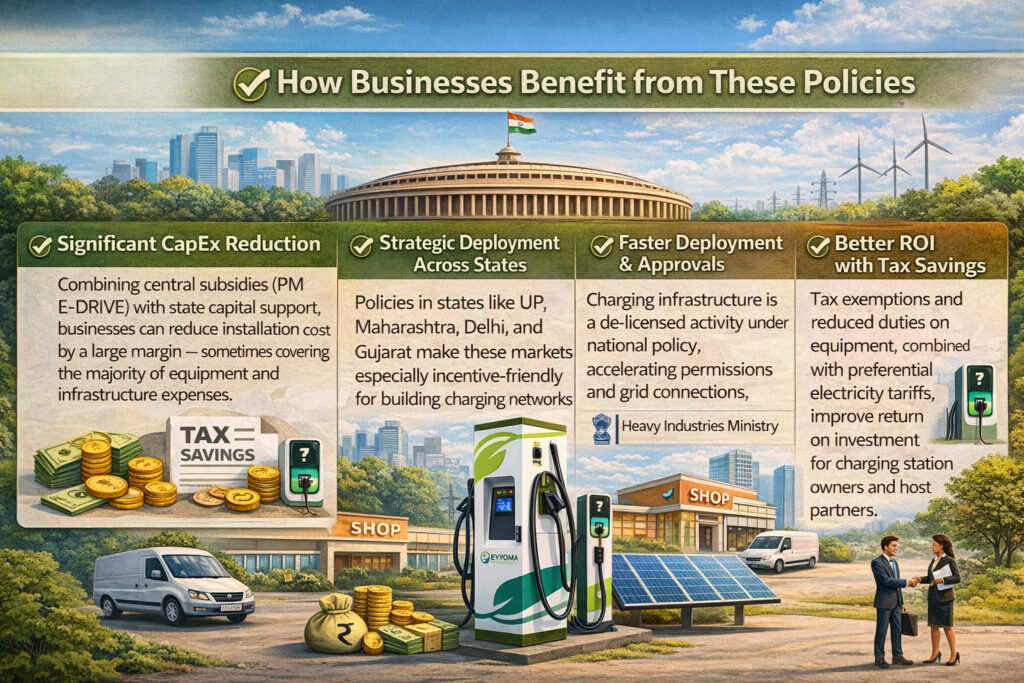

EV charging infrastructure allocation: ₹2,000 crore for pan India installation of public charging stations including highways and urban sites.

Charging stations are designated de licensed activities, enabling faster permissions and tariff setting.

So far, over 29,000 EV charging stations have been reported installed across India.

Under PM E-DRIVE, charging infrastructure subsidies are layered by category (public vs. private premises), with generous support for:

100% capital subsidy for chargers in government premises like stations, hospitals, airports.

Up to ~80% subsidy on infrastructure and 70% on charger equipment for private/commercial sites (e.g., malls, workplaces).

Tiered incentives depending on location and charger type (slow AC, fast DC) to ensure wide deployment.

State EV Policies: Extra Incentives for Charging Infrastructure

Beyond central schemes, many states provide additional rebates, capital subsidies, tax exemptions, and infrastructure support which can be stacked with national incentives for better economics.

Examples of Key State Incentives (2025)

Uttar Pradesh

Offers 20% subsidy on fixed capital investments for EV charging stations up to ₹10 lakh per station including upstream electrical infrastructure like transformers and grid connections.

Maharashtra

Implements Viability Gap Funding (VGF) of 15% reimbursement (up to ₹10 lakh) for DC fast chargers, especially along highways and in major urban centers like Mumbai and Pune.

Delhi

Provides 100% subsidy up to ₹6,000 per charging point for the first 30,000 installations at homes, apartments, and commercial locations.

Gujarat

Offers up to ₹10 lakh capital subsidy specifically for charging station installation along with registration fee waivers for EVs useful for charging networks at dealerships.

Odisha

The Government of Odisha unveiled its draft Electric Vehicle (EV) Policy 2025, targeting 50% EV adoption in all new vehicle registrations by 2030 a significant increase from earlier goals under the 2021 policy.

Tax and Duty Incentives

Lower GST and Duty Structures

EV chargers and associated equipment often attract lower tax rates relative to ICE equipment (chargers typically not burdened by high tariffs), helping reduce upfront capital costs.

EVs themselves benefit from a 5% GST rate, which indirectly improves charger usage economics by increasing EV sales.

Grid & Utility Benefits

Some state DISCOMs allow preferential electricity tariffs (Green Tariffs) for EV charging operations lowering operational costs.

Haryana and other states are moving toward tariff structures that benefit high capacity charging loads.

Market Context & Deployment Progress

India’s EV charging infrastructure is expanding rapidly:

According to the Ministry of Heavy Industries, over 29,000 EV charging stations are operational nationwide.

Charger density has increased nearly five times compared to three years prior — though utilization and uptime remain challenges in some regions.

Major industry players like Tata Motors and Tata Power are planning to scale networks significantly with both AC and DC fast chargers.

However, some planned government tenders — like Karnataka’s proposal for 2,500 PPP chargers — saw limited private participation, illustrating the importance of policy clarity and execution in successful deployment.

Conclusion: Opportunities for EV Charging Businesses

India’s policy landscape for EV charging infrastructure in 2025–26 is rich with financial support, state incentives, and tax benefits — making it an attractive period for EV charger manufacturers and ecosystem partners to scale:

Large central budgets under PM E-DRIVE reduce capital risk.

State subsidies stack with national schemes to further cut costs.

Tax and tariff advantages improve long-term economics.

Deployment targets and automotive commitments from manufacturers are signaling accelerating adoption.

For EVYOMA’s audience focusing on EV charger manufacturing, integration, and deployment understanding and strategically aligning with these policies will be a key competitive advantage.